Is it a Good Time to Buy a House?

Todd Craig

1/15/20262 min read

What History Tells Us About Housing Returns. Unpacking decades of data to understand the long-term outlook for real estate.

The question "Should I buy a house now?" is on the minds of many. With fluctuating interest rates and home prices, it's easy to get caught up in the short-term noise. But what does the long game look like for real estate? By examining decades of U.S. housing data, we can gain valuable insights into the resilience and potential of homeownership as an investment.

The Power of Patience: How Often Does Housing See Positive Returns?

Let's cut straight to the chase: when you look at housing over longer periods, the odds of a positive return skyrocket.

Here's a look at the odds of positive returns in housing over various timeframes, based on data since 1953:

1 Year: 89% chance of positive returns

3 Years: 92% chance of positive returns

5 Years: 93% chance of positive returns

10 Years: 98% chance of positive returns

15 Years: 100% chance of positive returns

The message here is clear: real estate tends to reward patience. While you might experience a down year or two, holding onto a property for a decade or more has historically almost guaranteed a positive return. Over 15 years, it's been a perfect track record.

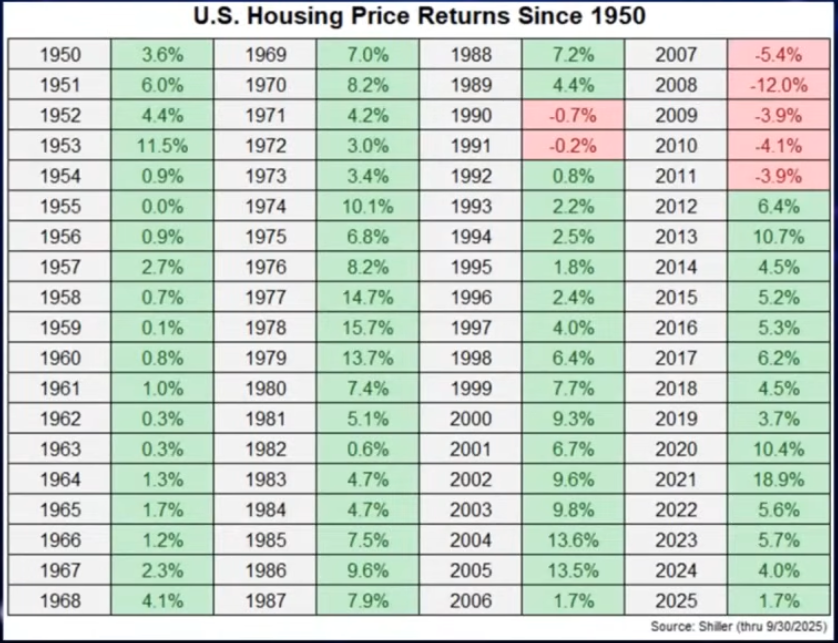

A Look Back: U.S. Housing Price Returns Since 1950

To truly appreciate the long-term trend, it's helpful to see the year-by-year performance. Since 1950, the U.S. housing market has largely trended upwards, with remarkable consistency.

For example:

1978 saw a robust 15.7% return.

2004 delivered 13.6% growth.

2021 experienced an impressive 18.9% surge.

Even during periods of economic uncertainty, housing has often bounced back. The most significant downturns, such as the -12.0% in 2008 during the Great Financial Crisis, are relatively rare and often followed by recovery. Minor dips, like the -0.7% in 1990, are even less common.

Most recently, returns for 2024 were 4.0%, with 2025 showing 1.7% through the third quarter, indicating continued, albeit slower, growth.

So, Should You Buy Now?

Based purely on historical data, the answer leans towards yes, if your financial situation allows for it and you plan to stay put for the long haul.

Here's why:

Long-Term Growth is Highly Probable: The data strongly suggests that over 10 to 15 years, real estate is a reliable investment for appreciation.

Inflation Hedge: Real estate often serves as a natural hedge against inflation, as property values and rents tend to rise with the cost of living.

Building Equity: Every mortgage payment helps you build equity, which is a form of forced savings.

Stability in Uncertainty: While markets fluctuate, the essential need for housing provides a foundational demand that keeps the market resilient over time.

Of course, buying a home is a personal decision that extends beyond just market data. Considerations like your job stability, current interest rates, local market conditions, and personal financial readiness all play a crucial role.

However, if you're worried about timing the market perfectly, history offers a comforting perspective: time in the market often beats timing the market. For those with a long-term perspective, buying a home has proven to be a sound financial move.

Charts courtesy of one of our favorite Podcast "The Compound and Friends". Subscribe here: youtube.com/@TheCompoundNews